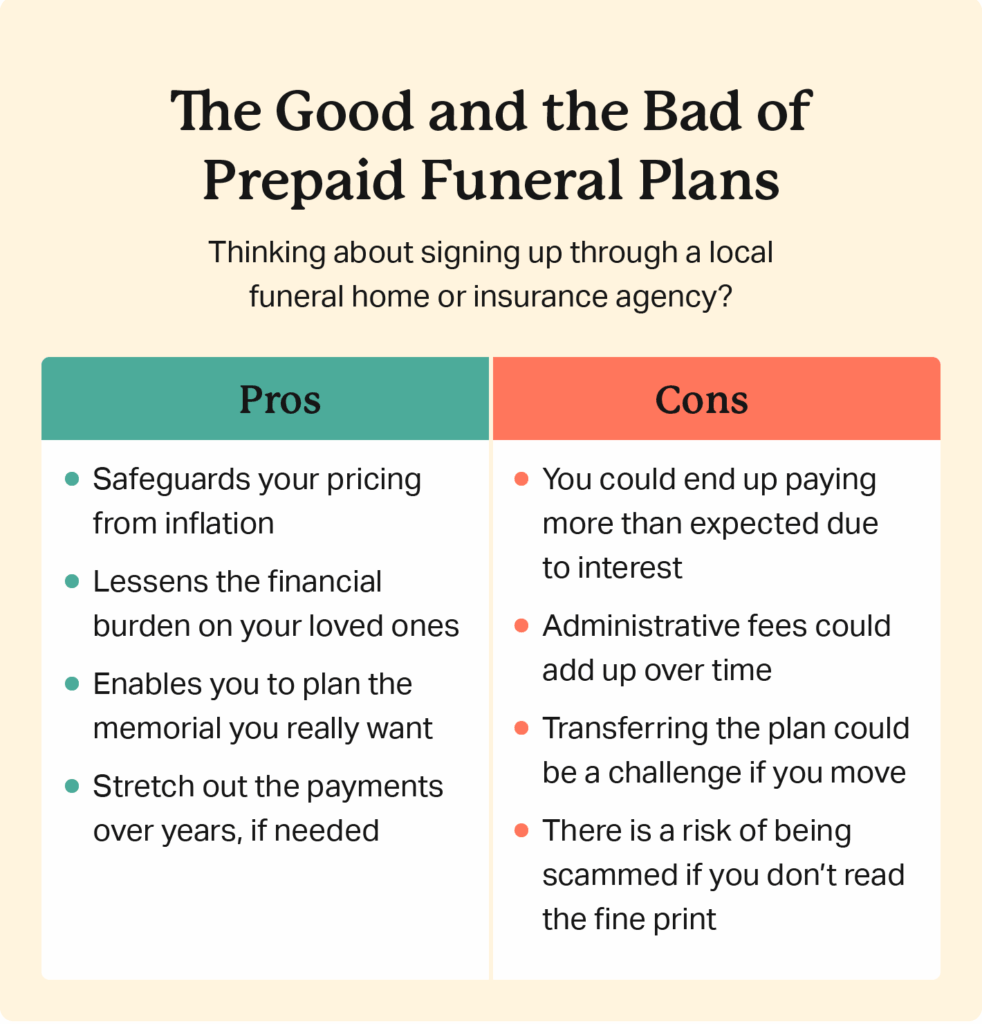

I get asked frequently why dont we sell funeral plans. The reason is until the industry offers true clarity to its clients, I do not wish to be promoting and selling something that doesn’t always live up to its promises at time of need.

While not yet a scandal on the scale of Payment Protection Insurance (PPI), concerns exist that prepaid funeral plans could become the next widespread issue due to mis-selling and lack of regulation. Several factors, including high-pressure sales tactics, consumer confusion about what’s covered, and a lack of proper regulation, have raised alarms within the industry and among consumer watchdogs.

Here’s why the comparison to PPI is being made:

- Mis-selling and High-Pressure Tactics:

Similar to the PPI scandal, there are reports of funeral plans being aggressively sold, with some consumers being pressured into buying plans they don’t fully understand or need.

- Lack of Consumer Understanding:

A significant number of consumers mistakenly believe their plans are regulated by the Financial Conduct Authority (FCA) (FCA) and that their money is fully protected, which is not always the case.

- Limited Regulation:

Before July 2022, the funeral plan market was largely unregulated, leaving consumers vulnerable to unscrupulous practices. While the FCA now regulates funeral plans, concerns remain about the transition period and the potential for past issues to resurface.

- Financial Risk:

Some providers have gone out of business, leaving consumers with plans that may not fully cover the cost of their funerals or with no recourse to recover their funds.

- Commission and Fees:

Concerns exist about high commission payments to intermediaries and the potential for plans to not represent fair value for money.

What’s being done?

- FCA Regulation: The FCA now regulates the funeral plan market, implementing new rules to ensure plans are sold fairly, perform as expected, and offer value for money.

- Banning Cold Calling: Cold calling by funeral plan providers has been banned.

- Improved Advertising Standards: New standards for advertising are in place to ensure plans are sold fairly.

- Commission Restrictions: Commission payments to intermediaries have been banned.

- Focus on Consumer Understanding: There’s a push for greater transparency and clarity in funeral plan marketing materials to ensure consumers understand what they are buying.

In conclusion, while the funeral plan market is not yet a full-blown scandal, the potential for consumer detriment is significant. The FCA’s increased oversight and focus on consumer protection are crucial steps in preventing a widespread issue similar to PPI.